Reflections on the First VC-Backed Bank Run

Much has been said about SVB’s failure. As a client of the bank for over two decades, first as an entrepreneur and then an investor, the…

Much has been said about SVB’s failure. As a client of the bank for over two decades, first as an entrepreneur and then an investor, the impact of its failure is comparable to what Michael Moritz so eloquently described as “a death in the family”: something to mourn and reflect on. By now the structural reasons behind its failure are well known. What interests me is the role it played in the technology ecosystem, and the role technology played in its demise.

The bank for founders

Startups are a hard bunch to bank: there are no assets to lend against. And many fail, often in spectacular fashion. SVB understood these needs. The bank underwrote against the risk profile of startups better than most, and leveraged its partnerships with venture firms to become the partner of choice for Venture Debt. Not surprisingly, startups and funds across the globe flocked to bank with SVB.

Fortunately, for the tech ecosystem, other institutions took notice. JPM recruited many of the failed bank’s leaders in recent years. And the Venture Debt asset class is now offered by many companies such as TriplePoint, Comerica, and Bridge Bank. Newer startups meanwhile have been flocking to Brex and Mercury, attracted by their modern products and founder-cenric perks. SVB was the first bank built for founders, but by the time of its collapse this month it was far from being the only one.

Herd mentality ..

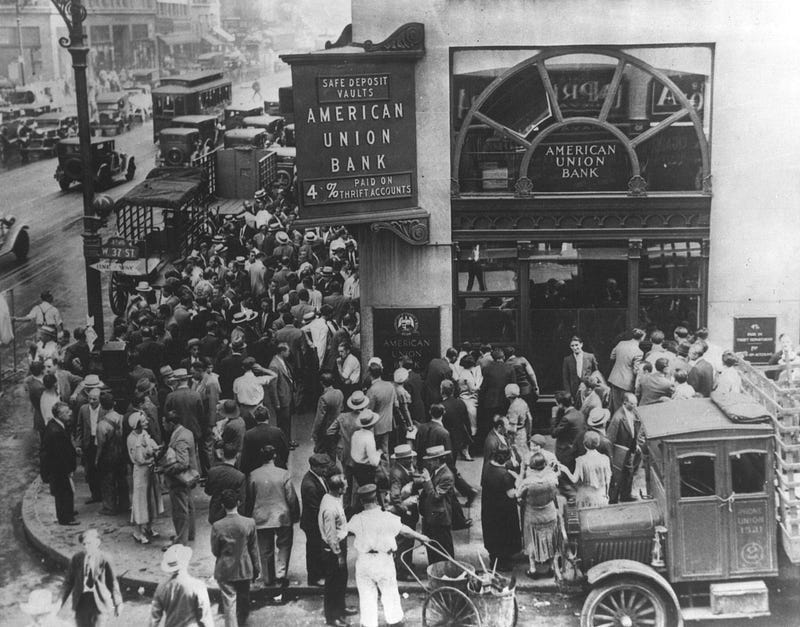

Still, SVB’s failure was epic. During the last major bank run on Washington Mutual in 2008, $15B of deposits were withdrawn in ten days. In the case of SVB, $42B of withdrawals were attempted in just a few hours. This frenzied behavior merits a pause. Herd mentality is an ancient human pulse. But technology put this impulse on warp speed.

When depositors mainly consist of startups backed by the same group of venture capitalists on their boards, and these venture capitalists all call their companies to let them know that others are withdrawing their funds from SVB, you end up with a textbook definition of a bank run. This was foolish. As Hemant Taneja of General Catalyst wrote: “causing a bank run at the most important institution in your sector can hardly be considered an act of fiduciary duty”

.. enabled by Technology

I am also surprised by how little attention has been given to the role technology played. This was truly the first Twitter-fueled bank run aided by mobile banking. Admittedly, SVB had the most tech-savvy clients today. But in a few years every bank will have depositors who are social media-obsessed and have two-factor authentication. The next bank failure will likely have a root cause other than government bonds held to maturity in a rising rate environment. But how it fails will likely look similar.

The need for circuit breakers

The FDIC were quick to respond by guaranteeing deposits and announcing a program shielding other banks from the risks of rising interest rates, the problem they understand and control. But they also need to re-instiute the friction in bank runs that technology has all but removed, for example via circuit breakers similar to the ones in the stock market.

The road ahead

The downfall of SVB will likely result in further tightening of the venture debt industry, making an already difficult year for funding even more challenging. But this will also create an environment where only the strongest and most innovative companies survive, leading to stronger startups with more profitable business models. SVB’s demise was a shock to the system, but sometimes a shock can be a good thing.